This Canadian apartment REIT is trading at 35% under NAV

Get exposure to some of Canada's most valuable real estate at a bargain price

In recent times, Canadian apartment REITs have experienced a massive correction with the one I am coving today being 50% off highs. An increase in interest rates hit them on two sides as cash flows got compressed from higher financing costs, and the yields became less attractive due to higher obtainable rates from fixed income. This is a fair reason for them to drop but they have since taken another leg down as rent growth has slowed a lot in Canada’s largest metros. In this piece I will explain why this decrease is likely to be temporary leading to great future returns for this REIT that is currently trading well below book and liquidation value.

The business

Minto Apartment REIT (which I will refer to as Minto) was founded in 2018, and it holds apartment buildings across Canada. They operate in the major centres of Ottawa, Toronto, Montreal, and Calgary. Some of their buildings are fully owned, and they also have partial ownership stakes in a few properties. Their effective number of units owned is 6,211. The market that the properties are in is quite important, as certain areas of Canada have conventionally traded at much lower cap rates than some of the smaller cities and the cities in the prairies (more about this in the next section).

The company also owns some convertible development loans, in which it provides financing to projects in exchange for a call option on ownership stakes (at 5% discounts to fair market values). These projects are by MPI (the company that manages the REIT). These loans currently carry a balance of ~129M, which represents around 5% of the company’s total assets.

Additionally, the company has properties under development in Toronto with completions expected in Q2 2026 and Q1 2027. The company also had some other projects in the works, which they canceled. I will discuss this further in the capital allocation section.

Canada Housing Market Economics

In general, housing in Canada’s major markets has been constrained. This is the result of a few factors, but it mainly comes down to housing starts not keeping pace with immigration. Cities like Toronto have had restrictive zoning policies, and they use development charges on new construction as a significant source of revenue. Currently development costs are believed to add over $50,000 to the cost of a one-bedroom condo. The large cities Minto operates in have also been the main destinations for immigrants. The Liberals just won another term as a minority government. Given that they can not form government on their own they will likely team up with the socialist NDP party again which will make the housing plan in Carney’s platform harder to execute since it provides subsidies to developers. One of the advisors to Carney is the head of an influential lobbying group called the Century Initiative, which wants to increase Canada’s population to 100M by the end of the century from the current level of ~41.5M, mainly through immigration. This chart, supplied by Minto, shows the population growth by year along with housing starts.

To reach a population of 100M by 2100, even assuming a flat replacement birth rate of 2 (much higher than the current rate of 1.4), 778k immigrants would have to arrive each year. While there is more of an imperative to increase housing starts, even hitting 400k is an ambitious goal. Mark Carney has set a target of just under 500k but this seems too optimistic. As evidenced by the valuation of this REIT there is a lot more pessimism among developers than there was in previous periods so even getting housing starts back to where they were in 2021 may not be possible. I will talk more about decreases in rents in the next paragraph, but it goes without saying that an environment with decreasing rents is hardly conducive to promoting investment in purpose-built rentals and there is a limit to how generous subsidies can be.

The reason for the population drop in 2025 and the projected drop in 2026 is that many people have been coming in via a visa type called TFW, which is mainly used by low-skilled workers, or by enrolling at diploma mills. There has recently been a crackdown, and some of these people will be granted permanent residency while others will be expected to leave the country. Canada has also restricted the pathways for immigration for international students upon graduation, decreasing enrollment even at the legitimate universities. This situation coupled with new condo supply from the ZIRP era coming online has led to a more competitive rental market where promotional activity like offering a month of free rent has become more commonplace. Minto has started occasionally offering this, but they prefer to do other concessions like offering free parking or storage when they have empty space. Many reports have been circulating like this one from rentals.ca that claims that rents for a 2 bedroom dropped nearly 10% y/y. While rents are down apartments are the least affected category with much larger drops seen in townhouses, condos and one-bedroom units. Minto says that they have seen much smaller drops and that their rents are closer to flat.

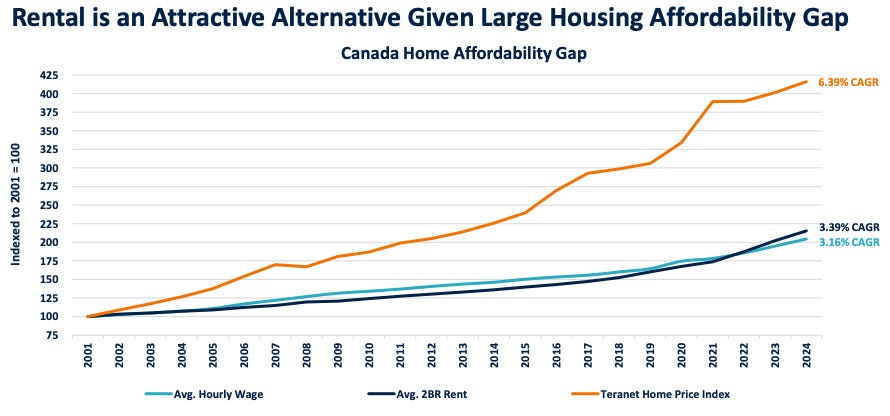

Another important measure is the increase in rents relative to the costs of home ownership. Since 2000, the average price of a detached house in Toronto has climbed from $250,000 to around $1.35M today, way outperforming most stock indices basically meaning that if you bought an investment property in 2000 with 5% down it was a hundred bagger. This performance continuing is highly unlikely, but the price movements created a lot of desire for residents of the city to yolo into the market, even though these days renting provides much lower housing costs unless you model in the value of a property you buy increasing a lot. Comparatively, rents have increased less, as shown in another chart provided by the company.

Many of the purpose-built rental buildings are quite old, as the last big construction wave for them happened in the 70s. Recently, Condo construction has been much larger but given that they were bought for investment purposes in many cases, they still provide real competition to the company’s buildings. My other point here is that in markets like Toronto, Ottawa and Vancouver (Calgary is more affordable) the monthly costs of owning a given unit vs renting it are much higher and as such, someone buying a condo for investment purposes will have to cover a large portion of the mortgage with their own capital.

Additionally, Ontario (the province containing Toronto and Ottawa) has had rent control in place. The rent control is structured such that rent can only be increased for a tenant by 2.5% per year, and no-fault evictions are also prohibited, apart from in a few circumstances. The relevant circumstance for the REIT is that you can do an eviction if renovations need to be done on the unit, although the REIT says that they don’t use this strategy to evict under-market tenants. Once a tenant is gone, rent can be raised as much as the landlord wants. The other important wrinkle is that in 2018, the Ontario government made a rule that buildings completed after 2018 are not subject to rent control. Overall, it is a risk that increases upon a tenant leaving, could become prohibited, or the exemption for post-2018 buildings could be removed eventually.

Rent control creates a dynamic where turnover is much higher in Calgary, as there is no rent control. Calgary also has far more affordable homes for sale, so there are many more temporary renters. Across the portfolio, the company estimates that there is a lease-to-gain potential of 13% relative to current rents charged.

Montreal has less stringent rent control, and BC has rent control, but I won’t get into the details since it is a smaller market for Minto.

In conclusion, if immigration ramps up again rents should start to rise again. If rents don’t show increases again then there will be little appetite to build purpose-built rentals. The current dynamic is being caused by a lagging effect and investors extrapolating the rent declines into the future is one of the key reasons that Minto stock is available for the current bargain price. It is basically the chicken and egg problem for renters and Minto is the key beneficiary.

Assets

As you can see in the table, the properties in the portfolio are fairly dated, with most going back to the apartment construction boom of the 1970s but this is actually newer than most of the supply in the purpose-built apartment market.

The other feature that I touched on earlier is that rents per unit are higher and cap rates are higher as well for the properties in Toronto and Ottawa. The company does not provide cap rates for individual properties, but the rates range from 3.75% to 5.13%, with a weighted average of 4.32% as of December, up from 4.16% in the previous year. The properties are revalued each year, considering market conditions to calculate cap rates and expected rental incomes and that is how their carrying value is calculated. Management has stated that they believe that the entire portfolio could be sold for its carrying value, but blindly following management’s NAV calculations has caused problems for REIT investors before; just look at some of the office REITs. In the longer run the cap rates will reflect some of the factors I mentioned above. In Canadian politics Toronto is an extremely important area as it can swing Liberal or Conservative and due to the first past the post system it holds the balance of power. Given that older people are higher propensity voters it is not in the interest of a government to cause property values to drop too dramatically.

Debt

The debt side of the balance sheet for the company is overcomplicated largely due to the accounting rules in Canada. The main confusing part are the Class B and Class C units. The class B units are basically the same as the standard publicly traded class A units except they are just owned by MPI. These are convertible to Class A units, and they are entitled to the same dividends as the Class A units but for some reason the dividends paid are counted in interest expense. Also, a gain is booked when the value of the Class A unit falls and a loss is booked when the units rise. I just factor this into the share count and ignore the fake expenses. The class C is legitimate debt as it reflects compensation due to MPI since for some of the jointly owned properties the debt is guaranteed by MPI. The carrying values of the Class C units represent the PV of payments due to MPI under these mortgages.

Other than that, the only substantial debt is mortgages which are all fixed and have a diverse schedule of maturities.

In total the debt is around $1.1B.

Capital Allocation and Strategy

Historically, there have been 4 major uses of capital for the company: 1. Issuing Construction development loans, 2. Exercising purchase options on the CDLs, 3. Purchasing properties in the market and 4. The dividend. The dividend is likely to continue going forward, but the company has stated that they are putting the brakes on issuing any more CDLs, and they have decided not to exercise some of their options. As these CDS roll off, management has said that they are likely to deploy the proceeds into their share buyback program that was recently initiated.

In accordance with TSX rules the total buyback authorization is only for 10% of the float (which excludes Class B) but there is also the option for the company to negotiate a repurchase of class B units from MPI. If a deal can’t be reached then the company could issue a tender offer. The strategy makes sense as it would not make sense to buy properties at the market value when, via buybacks, they can purchase properties at below market rates. They also pay a dividend, and the units have a modest yield of 4%, but they have a low payout ratio. The dividend is paid monthly which doesn’t matter to me but it tends to be appreciated by retirees. The nice thing about the buybacks is that the fewer units there are outstanding, the fewer dividends are being paid, so if the stock does not respond management can increase the pace at which they are buying shares.

Valuation

Due to the issues with the class B units and fair values gains and losses affecting the financial statements it is useful to use adjusted FFO as a proxy for earnings. This metric can be affected by one off factor since the rentals include utilities so weather can affect utility expense. The company also pays for snow clearing so bad winters can skew this metric as well. The metric includes a Capex reserve of just over $6M a year. When you adjust for the Class B units you get an equity value of ~$860M and TTM adj FFO is $58.3M implying a cap rate of 6.8%, well below market comps and the company’s mark of 4.32%. This report from Avison Young puts average cap rates for 2024 multi-family building sales in the Toronto area at 4.2%. For H1 2024 they saw Ottawa multifamily transactions at a 4.75% cap. To be conservative I put the portfolio at a 5% cap.

A 5% cap puts the portfolio’s value at 35% higher than the stock is currently trading. Given capital allocation being sensible I believe that the stock is attractive and has fairly limited downside given where cap rates currently are. There is additional upside if cap rates rise. Buying back shares at this valuation sweetens the deal further.

Conclusion

In short given the smart capital allocation priorities and pessimistic assumptions regarding rent growth there is significant potential for this stock to outperform. It is particularly attractive for me and other investors holding the stock in Canadian registered accounts as there are no taxes charged on the distributions. Given the fairly low payout ratio, it is still a fine holding for some international investors as well since the withholding taxes won’t weigh too heavily on returns.

Another attractive Canadian apartment REIT that is also trading at a steep discount to NAV is Northview apartment REIT which has far more exposure to higher cap rate markets, as such it does generate more FFO/share than Minto. I hold Minto and am planning on acquiring some shares in Northview as well. This will provide more diversification and parts of the Minto thesis are applicable to Northview as well.